Supply

Fixed issuance

Bitcoin's monetary policy is public, mechanical, and enforced by the network. No emergency meeting can create the twenty-two millionth coin. The supply schedule is a fact of the protocol, not a policy preference.

Bitcoin is not a stock, a payment app, or a faster version of banking. It is a monetary protocol built on a single insight: the rules that govern money should not be changeable by the institutions that benefit from changing them. This guide builds from that premise outward.

Most people arrive at Bitcoin through its price. That is the least useful entry point. A thousand-percent return tells you nothing about the mechanism, and without the mechanism, volatility looks like randomness rather than signal.

The better question is older and simpler. What happens to a society when the rules governing its money can be quietly rewritten by the institutions closest to that money? What happens to savings, to planning horizons, to the relationship between effort and reward, when the unit used to store value is systematically expanded by parties who benefit from that expansion? And if that describes the current arrangement — which it does — what would a credible alternative actually look like?

This guide is the path through those questions. It does not start with Bitcoin. It starts with money, because that is where the argument lives. Bitcoin is the answer to a problem that most people have not been taught to name. The six parts that follow name the problem, explain the mechanism, and then describe what Bitcoin actually is and why the specific properties it has — not its price, not its adoption curve — are what matter.

Money has three jobs. It stores value across time. It moves value across space. And it prices value between strangers who have never met and never will. When it performs all three reliably, a society can defer consumption, plan across decades, and coordinate at a scale that no single institution could manage by itself. When it fails any of them, the damage starts quietly and becomes structural.

The store-of-value function is the one that fails first under inflationary regimes, and the most consequential for ordinary people. If the money sitting in your account reliably loses purchasing power year after year, the rational response is not to save. It is to spend now, borrow against the future, or find an asset that holds value better than the currency itself. This is not irresponsible behaviour. It is the logical adaptation to a monetary environment where patience is systematically punished.

Walk that logic forward a generation. An economy where saving is irrational produces an economy shaped by leverage, asset speculation, and the consumption of future output to fund present demand. Debt-to-GDP ratios climb. Private credit expands into increasingly fragile structures. The institutions designed to manage monetary stability become the institutions most exposed to its failure. Each cycle requires a larger intervention to produce the same stabilisation. The system does not collapse — it compounds.

The medium-of-exchange function is the one governments most frequently invoke to defend fiat systems. The argument is that money must be elastic: supply must expand to meet economic need, smooth contractions, and prevent deflationary spirals. This is not wrong on its face. The problem is that monetary elasticity is never genuinely neutral in its distribution. The question of who decides when supply expands, by how much, and whose liabilities are backstopped in a crisis is not a technical question settled by economists. It is a political question answered by the institutions closest to the mechanism. The consequences of that arrangement are the subject of Part Two.

The unit-of-account function — the ability to price things accurately — is the most subtle failure mode and the hardest to perceive in real time. When the money supply expands unevenly, relative prices shift in ways that obscure genuine signals about scarcity and value. Capital gets directed toward assets that look productive in nominal terms but are simply rising with money supply. The misallocation is invisible in the short term and structural in the long term. It produces boom-and-bust cycles that look like random market events but are the predictable consequence of price signals corrupted by monetary distortion.

None of this requires a conspiracy. It requires only that the incentives of the institutions controlling money supply point consistently in one direction, and that there is no external constraint strong enough to resist them across political cycles. Sound money — money that is hard to produce and impossible to expand arbitrarily — was historically that constraint. The question Bitcoin asks is whether that constraint can be reinstated without relying on the trust of any institution to maintain it.

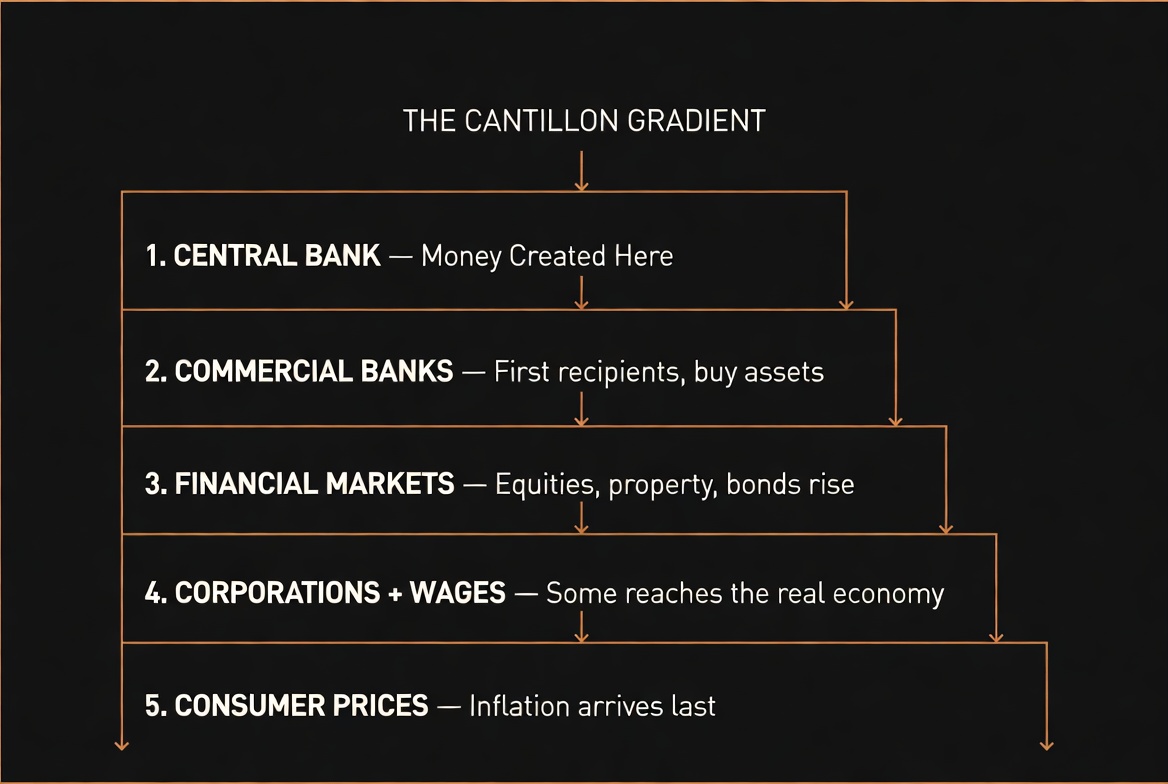

Richard Cantillon was an Irish-French economist writing in the early eighteenth century, long before central banks existed in their modern form. The observation attributed to him is the most important thing most people have never been taught about money: new money does not enter an economy evenly. It moves through institutions first, then asset markets, then wages, then consumer prices. By the time ordinary savers see any effect from monetary expansion, the transfer has already happened.

The gradient works like this. A central bank creates new money — through quantitative easing, emergency lending facilities, or government bond purchases. The first recipients are financial institutions. They use that money to buy assets before prices adjust: equities, property, bonds, private credit. Asset prices rise. The balance sheets of those institutions improve. The collateral against which they can borrow more improves. They acquire more assets. The cycle reinforces itself.

Eventually, some portion of this filters into the real economy through employment, wages, and credit availability. By this point, the asset price inflation is already embedded. The person who owned assets before the expansion holds more in real terms. The person who held cash savings holds less. No explicit transaction moved value from one to the other. The mechanism is price-level change operating differently on differently-positioned balance sheets. The outcome looks like inequality widening for reasons no one can quite name.

This is not a partisan observation. It is a description of arithmetic. It explains why every significant cycle of monetary expansion since 2008 has reliably widened the gap between asset-holders and wage-earners. Why central bank balance sheet expansion correlates so consistently with equity market performance rather than median wage growth. Why the political anger directed at economic inequality tends to find visible targets — specific corporations, executives, immigration, trade policy — while the underlying monetary mechanism, which is the actual engine of the divergence, is rarely named in the same conversation.

The reason it is rarely named is not complicated. The institutions with the most influence over economic discourse are also the institutions most proximate to the creation mechanism. Central banks, major commercial banks, large asset managers, government treasuries: all of these sit at the top of the gradient. None of them has a strong institutional interest in making the mechanism legible to the people at the bottom of it.

Bitcoin matters here because it removes the central point of discretion. There is no equivalent of a central bank deciding when to expand supply, by how much, in response to which political pressures. The supply schedule is public, mechanical, and enforced by the network. New Bitcoin is issued on a known schedule that tightens every four years regardless of economic conditions, political circumstances, or institutional preference. The gradient requires a discretionary tap at the top. Bitcoin does not have one.

A 10–12 minute audio overview of Parts One and Two — the fiat money problem and the Cantillon Effect — generated by NotebookLM and designed for someone who has never questioned how money creation works. Create it once, share it as a YouTube audio upload, paste the embed below.

Scarcity only functions as a monetary property when it is enforceable. An asset can be declared rare. It can be culturally treated as precious. But unless there is a mechanism that physically or architecturally prevents supply expansion, any declaration of scarcity is ultimately subject to revision under sufficient political or economic pressure. The history of monetary systems is largely the history of that revision happening, repeatedly, at exactly the moment when the pressure is highest.

Gold was the most credible attempt at enforced scarcity in the pre-digital world. The rate at which it can be mined is constrained by geology: finding, extracting, and refining gold requires significant physical effort and capital. No single actor can unilaterally increase the supply. This made gold a reliable store of value across centuries and across wildly different political systems. Its scarcity was not a convention that could be voted away. It was a property of matter.

The problem with gold as a monetary foundation in the twentieth century was not its scarcity. It was the trust required at scale. When enough value is stored in gold, it migrates from physical metal to certificates, then to financial claims that represent the metal without requiring direct possession. Those claims can be — and historically have been — diluted, suspended, or confiscated. The United States suspended gold convertibility in 1933 and ended the Bretton Woods gold standard in 1971. The constraint that had disciplined monetary policy for decades was removed by executive order on a single afternoon. The physical scarcity of gold was intact. The institutional layer on top of it was not.

Bitcoin's scarcity is architectural rather than physical. The supply schedule — a maximum of 21 million coins, with new issuance halving roughly every four years until the final fraction is mined sometime around 2140 — is encoded in the protocol that every node in the network runs. It is not a policy decision subject to committee review. It is not a target that can be quietly revised when the political pressure is high enough. Changing it would require the coordinated consensus of the entire global network of nodes and miners, all of whom have strong economic incentives against any such change. The constraint is not held in trust by any institution. It is enforced by the collective self-interest of every participant.

The halving mechanism makes this tangible in real time. Every four years, the block reward — the new Bitcoin issued to miners who process transactions — cuts in half. The rate of new supply decreases on a publicly known schedule, years in advance. In April 2024, the fourth halving reduced the daily issuance from around 900 Bitcoin to 450. The fifth will reduce it again in 2028. This is the inverse of emergency monetary policy, which typically accelerates supply precisely when confidence in the system is lowest. Bitcoin tightens supply on a schedule that is indifferent to economic conditions, political cycles, and institutional preferences.

The number 21 million is not branding. It is not a marketing decision made by an early developer to create artificial scarcity. It is the constraint that the entire monetary argument rests on. Remove it, and Bitcoin becomes another programmable digital asset with flexible issuance — useful perhaps, but not categorically different from what already exists. Keep it, and it is the first monetary instrument in recorded history where the supply rules are not held in trust by any institution that could benefit from revising them.

A deeper audio dive into Part Three and the broader Bitcoin architecture — for readers who finished Parts One and Two and want the mechanism explained in full. Uses the Bitcoin Whitepaper and The Bitcoin Standard as primary sources.

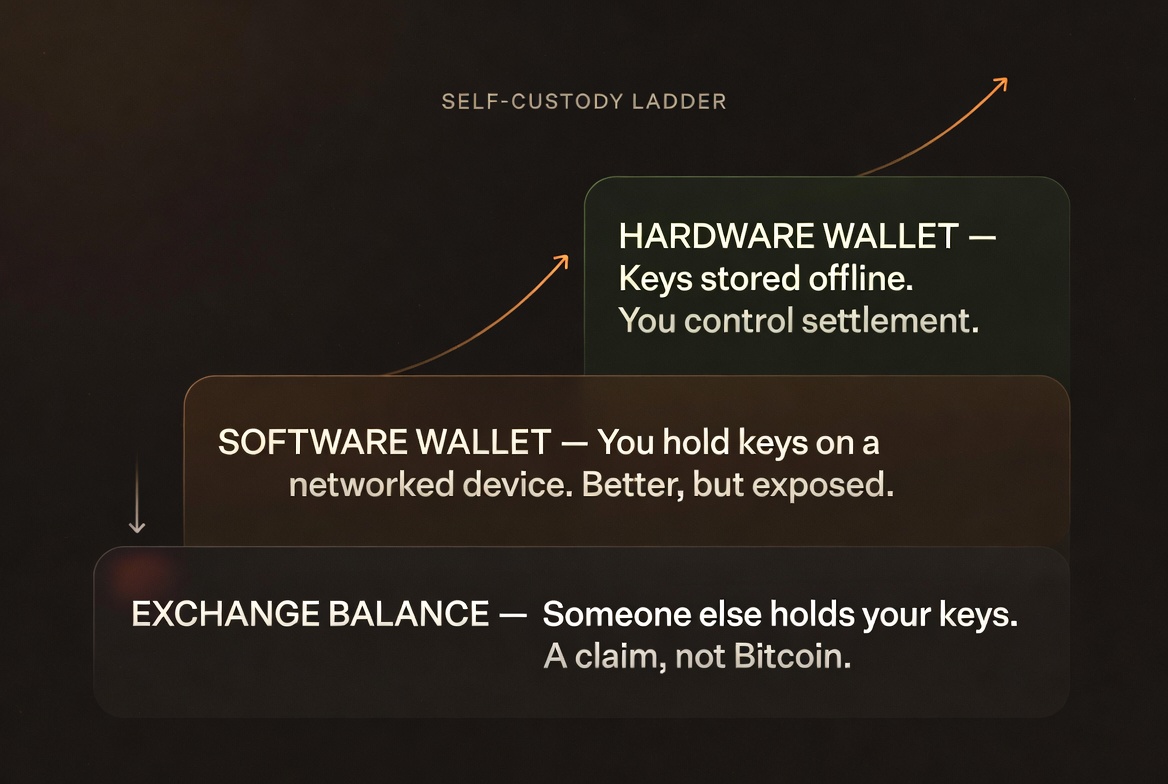

Owning Bitcoin means understanding the difference between price exposure, an exchange balance, and holding your own keys. Seed phrases, hardware wallets, Lightning wallets, and inheritance planning — explained without the religion. The aim is competence. The line between a permission slip and an asset is a twelve-word phrase.

Most of what is marketed under the banner of cryptocurrency recreates exactly the problems Bitcoin was built to escape: insiders, pre-mines, monetary discretion, governance capture, and marketing narratives written to obscure the mechanism. The category separation matters because conflating them leads to the wrong conclusions about what Bitcoin's properties actually are and why they are hard to reproduce.

Exit is not a fantasy or a political statement. It is the capacity to move value, speech, identity, and work outside institutional systems that increasingly demand obedience before service. Bitcoin is one layer of that capacity — not sufficient on its own, but a necessary component for anyone building a life that does not depend on the continued goodwill of institutions whose incentives are not aligned with your own.

Bitcoin's monetary policy is public, mechanical, and enforced by the network. No emergency meeting can create the twenty-two millionth coin. The supply schedule is a fact of the protocol, not a policy preference.

The base layer is slow by design. It prioritises settlement certainty over convenience. A confirmed transaction is final. No institution can reverse it, freeze it, or demand identification before allowing it.

A balance on an exchange is a claim on Bitcoin. A private key is Bitcoin. The distinction becomes decisive when institutions are stressed, regulated, or ordered to restrict access.

Bitcoin converts real energy into settlement security. That cost is not waste by default. It is the mechanism that makes rewriting history economically prohibitive. Security without a trusted third party requires an external anchor.

When money holds value reliably, saving becomes rational. Long planning horizons become possible. The structures that require multi-generational patience — infrastructure, institutions, families — become viable again.

Bitcoin's price is volatile because the market is continuously repricing a new monetary asset against a world priced in inflating fiat. Volatility in the price layer is not evidence of failure in the monetary layer. They are different things.

Gilt yields above 5%, $1.8 trillion in gated redemptions, private credit under pressure, and the Iran shock as structural accelerant. The current case for Bitcoin and gold as monetary escape valves — made through the data, not the ideology.

Bitcoin as geopolitical signal: price shock, strategic adoption, and monetary repricing inside a wider institutional fracture. How the same seventy-two hour window told a different story depending on which layer you read.

How Iran weaponised the Strait of Hormuz and broke the safe-haven assumption. Hormuz traffic down 97%, gilts above 5%, $2.5 trillion wiped from global bonds. The macro regime shift and what it means for hard assets.

Live prices, the BTC/gold ratio, bond yields, debt-to-GDP, and the AI capability index. The dashboard is the quantitative layer underneath the analytical framework.

Satoshi Nakamoto, 2008. Nine pages. The entire system described. Available free at bitcoin.org/bitcoin.pdf — read it once you have finished the learning path here. It is shorter and more readable than most people expect.

Saifedean Ammous, 2018. The most coherent single-volume argument for Bitcoin as sound money. Chapters 1–5 cover the monetary history that frames everything else. Start there before the later technical sections.

Yan Pritzker, 2019. Fifty pages. The best plain-English explanation of how Bitcoin actually works at a technical level — proof of work, mining, keys, and the blockchain — without requiring any prior technical knowledge.